Partnership. Expertise. Commitment.

Our industry experts provide insurance coverage, services and solutions tailored to meet your specific needs.

Effective risk management for warehousing is both broad in scope and also needs to take into account the cascade effect often involved in the losses claimed under the business's insurance. For this reason it's important for industry operators to ensure they have damage mitigation planning in place, and that their insurance covers them for all of the potential exposures that apply to the property.

These range from the security of the building itself to the contents being stored. The information in this article has been adapted from Gallagher business partner QBE sources which show that

To reduce potential losses and business disruption it pays to put mitigation measures in place, and there are a number of factors to take into consideration in respect to your particular property.

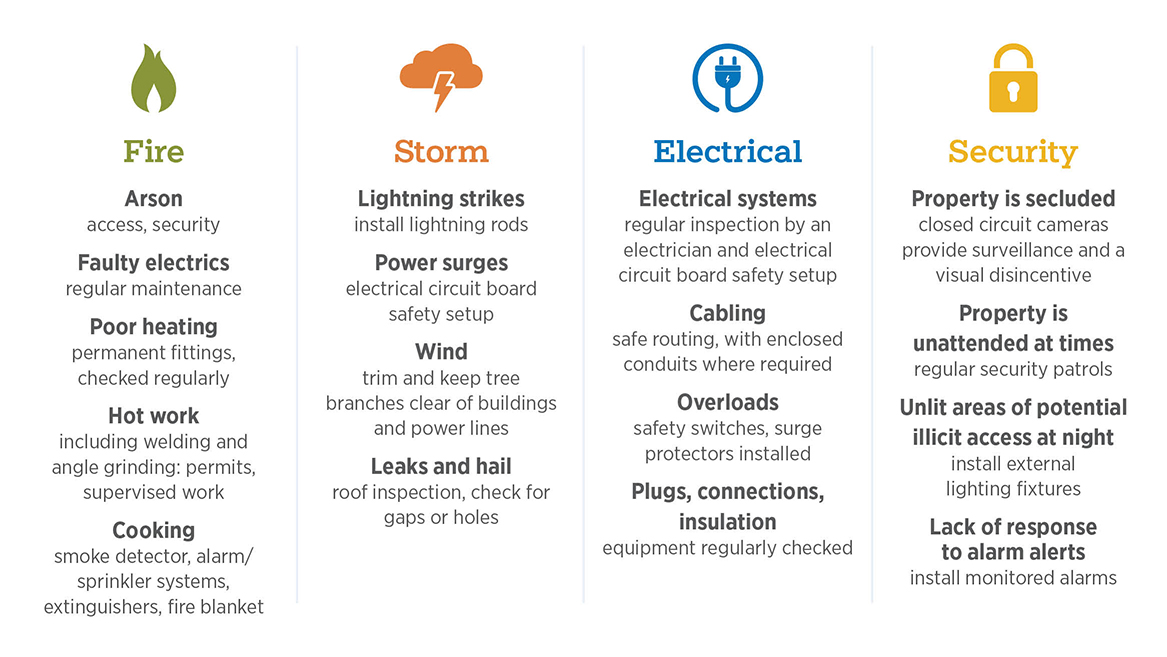

The age, condition and usage of the building provide the basis for your risk management approach. Some buildings may present greater risks in terms of water damage, for example.

Materials should also be taken into account. If asbestos has been used in the construction the costs involved with containing contamination and remediation should be factored into your sums insured.

Similarly in the case of food storage or refrigeration areas insulated with expanded polystyrene (EPS), or highly flammable aluminium composite panels (ACP) in external cladding, the fire risk will be higher so increased prevention and containment measures, through sprinkler systems, for example, are necessary.

Is your warehouse part of a business complex or in proximity to other business properties, as in an industrial park? In this case you need to plan for site containment that limits the possibility of fire spreading.

Looking at the internal layout of your warehouse with a view to locking down discrete areas and ignition sources can help minimise damage to stock and interruption to business operations.

The types of goods in storage also dictate the risk management protocols required. Are they or their components or packaging

What form are they in? Aerosols and liquids enable fires to spread more quickly.

Do they contain batteries, which are possible sources of ignition?

Analysis of the material being stored should inform how it's stored and contained to limit damage potential.

How goods are stored, especially in relation to containment measures such as fixed sprinkler systems, can also influence how effective your risk management measures are likely to be.

Typical storage hazards include

The movement of goods to different areas can also effect the efficacy of risk management measures and this needs to be a consideration in the internal warehouse layout as well.

Electrical issues are a significant cause of warehouse fire claims, and include

Planning for regular maintenance updates, electrical checks and thermographic scans can help you to identify potential trouble spots before they become problematic.

Water damage is a significant loss trigger in warehouse insurance claims and while some events are due to storms and flooding, others are caused by poor building maintenance. With this in mind, make roofing and guttering inspections part of your regular property upkeep.

Smoke can also cause a substantial amount of damage, rendering goods unsaleable. Separating out discrete areas to enable fire containment can help minimise smoke damage.

Because both are potentially combustible, waste disposal and pallet storage should be part of your site organisation. Considerations might include the construction material of any adjacent walls as well as the pallets (wood or plastic), and the height they are stacked to. QBE recommends separating pallets by 10 metres from warehouse walls.

As a first step in your risk management planning consider conducting an audit to identify the exposures on your site.

In terms of general essentials minimum requirements might include

By periodically reviewing your warehouse and storage risks and implementing effective loss prevention procedures and protection systems where necessary, you can support your insurance program and reduce the possibility of suffering losses or having to suspend operations.

Awareness of these exposures enables you to develop risk management or safety protocols which you can document and deploy. Having daily and monthly checklists helps reinforce observation of the protocols.

Some activities may require their own set of procedures, such as pallet management, goods handling, storage, hot work, electrical systems, dust accumulation and staff smoking arrangements.

Taking these actions helps provide your insurer with the assurance that you are being proactive about risk management in your business, making your enterprise a more attractive insurance prospect and improving your chances of securing more favourable terms on your cover.

Commercial property risks and insurances can be one of the most critical areas of focus for a business. As a high value asset and high cost risk, expertise and support from a broker is of critical value.

Gallagher provides insurance, risk management and benefits consulting services for clients in response to both known and unknown risk exposures. When providing analysis and recommendations regarding potential insurance coverage, potential claims and/or operational strategy in response to national emergencies (including health crises), we do so from an insurance and/or risk management perspective, and offer broad information about risk mitigation, loss control strategy and potential claim exposures. We have prepared this commentary and other news alerts for general information purposes only and the material is not intended to be, nor should it be interpreted as, legal or client-specific risk management advice. General insurance descriptions contained herein do not include complete insurance policy definitions, terms and/or conditions, and should not be relied on for coverage interpretation. The information may not include current governmental or insurance developments, is provided without knowledge of the individual recipient's industry or specific business or coverage circumstances, and in no way reflects or promises to provide insurance coverage outcomes that only insurance carriers' control.

Gallagher publications may contain links to non-Gallagher websites that are created and controlled by other organisations. We claim no responsibility for the content of any linked website, or any link contained therein. The inclusion of any link does not imply endorsement by Gallagher, as we have no responsibility for information referenced in material owned and controlled by other parties. Gallagher strongly encourages you to review any separate terms of use and privacy policies governing use of these third party websites and resources.

Insurance brokerage and related services to be provided by Arthur J. Gallagher & Co (Aus) Limited (ABN 34 005 543 920). Australian Financial Services License (AFSL) No. 238312